Whether it’s for profit, or just for the love of the game, NFT trading is more popular than ever – but where are our precious NFTs actually stored? These days, owning NFTs can be a sign of opulence too. Everybody wants to flex their success in the market, but there’s one question they never ask:

Could these precious digital assets disappear one day?

Well, maybe. The answer isn’t so straightforward and requires us to first break down the storage options for both NFT creators and NFT holders.

How do NFTs actually work?

In order to understand NFT storage options, we must first understand what they are.

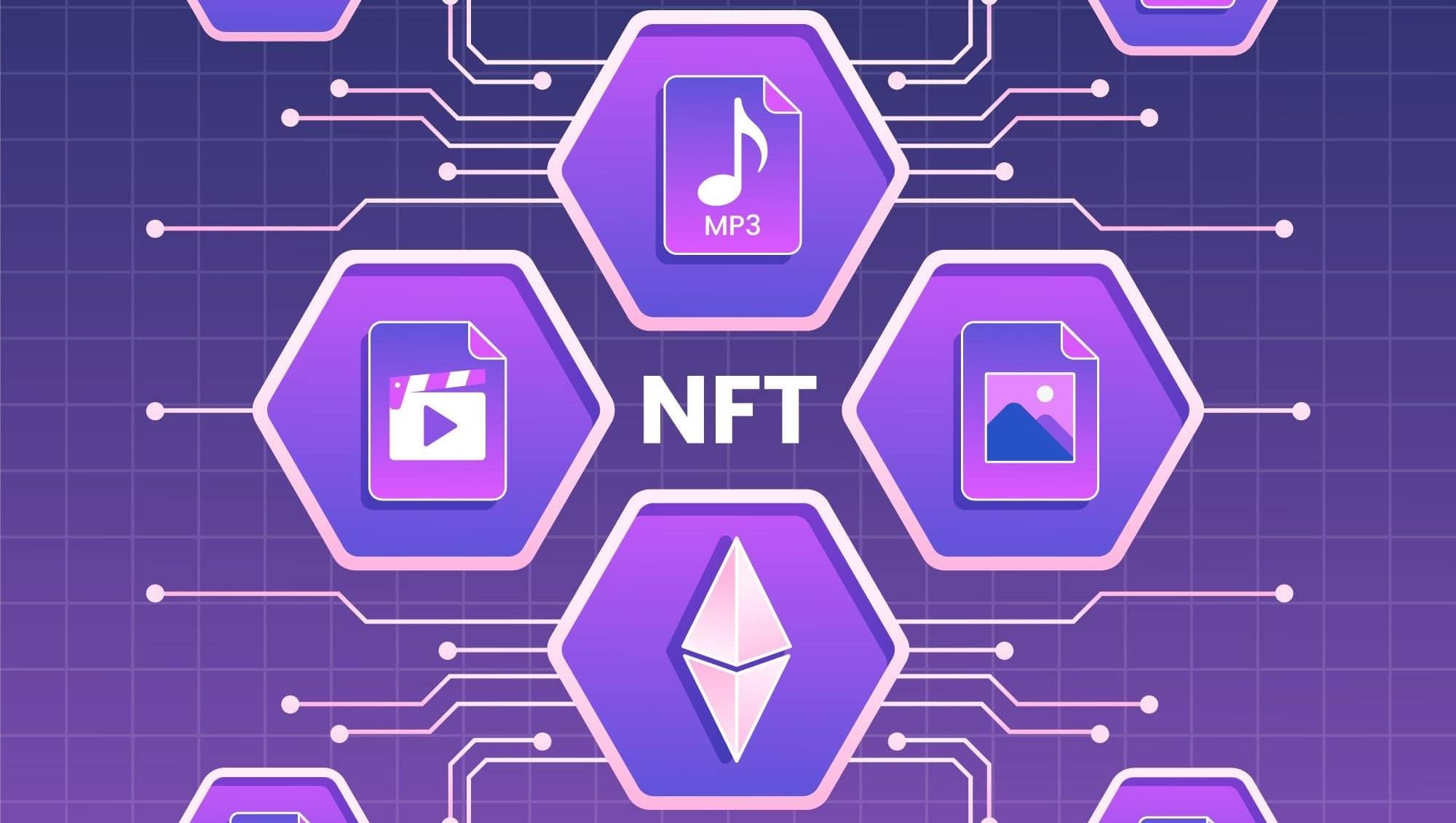

In essence, Non-Fungible Tokens are virtual representations of an asset. These tokens are provably unique and non-interchangeable. This means we can’t swap them like cryptocurrencies, which are all equal.

An NFT can represent any digital or physical asset, including music, movies, fine wine, and even real estate. Connecting the two involves creating a smart contract, which manages token ownership and transferability.

Now, most NFT smart contracts are based on the Ethereum ERC-721 standard. As a result, the code for each smart contract is stored on the blockchain – and it’s not going anywhere.

Meanwhile, the content associated with the smart contract is often stored somewhere else – and that’s the main problem.

Here’s an example: you’ve just bought an ape NFT. You own it, which is provable through the Ethereum smart contract. That smart contract will stay on the blockchain, letting everybody know where, and when, the digital content was minted.

However, the JPEG file associated with the smart contract – in this case, your ape cartoon – can be stored anywhere else on the internet. And yes, this means it could disappear, depending on where it is.

So then the next question becomes – where is the safest place to store NFTs?

How to store an NFT safely?

As noted above, we can store NFT metadata and content anywhere on the internet. For example, a project may store its collectibles via an HTTP URL. If for any reason somebody alters that URL, your precious JPEG, song, or other types of digital asset, is gone for good.

In other words, if an NFT creator decided to shut down their project for whatever reason, all of their NFT holders could lose their digital assets and accompanying metadata.

It’s a shocking possibility, considering the millions of dollars invested in NFTs so far. Of course, it’s unlikely for big projects like BAYC, but for a new one? It could happen.

William Entriken, the author of ERC-721, explains that this issue has been ‘outside of the scope’ for the team of Ethereum developers:

“Who is the authority and who owns what and can we prove that? This is a little bit outside of the scope of the standard,” he said.

Of course, hackers can attack NFTs too. In fact, marketplaces like Nifty Gateway had to deal with hacking, and their users lost thousands of dollars as a result.

But how can we make sure that our precious digital content isn’t going to disappear by magic?

Where do NFT creators store their creations?

Given the fundamental importance of decentralization to the NFT space, it should come as no surprise that storing NFT files in centralized servers is by far the least desirable option. For one thing, it makes NFT assets more vulnerable to being lost or corrupted. While some projects do this, or at least start off this way, there are really two respectable options for NFT creators these days.

NFTs stored on-chain

Some NFTs are stored completely on-chain. In short, on-chain NFTs are completely written onto the blockchain, complete with their smart contracts and metadata.

In some ways, this is the optimal way to store NFTs. It takes advantage of the best features of the blockchain, storing complete NFT information on a secure, decentralized network. The downside is that storing that much information on-chain can be pricey, especially if the tokens themselves have large file sizes.

Nevertheless, some NFT projects have managed to pull off putting their entire collections on chain. CryptoPunks would be the primary example. Indeed, while they were initially stored off-chain, Larva Labs moved the collection to be fully on-chain in August 2021. Other big examples of on-chain NFTs are Loot, Autoglyphs, Nouns, and Avastars.

NFTs stored On IPFS Or Arweave

Many NFTs have files that are too large or too expensive to store on proof-of-work blockchains like Ethereum. In that case, these NFTs will use a decentralized hosting service like IPFS (InterPlanetary File System) or Arweave to store their NFTs.

When you’re using IPFS, your NFTs are stored off-chain. This option is using an identification code (CID) linked to the content of your NFT. This type of data can’t be modified (unlike an URL, which can be changed anytime).

Where can collectors store their NFTs?

So where NFT creators store collection assets is one thing, but how about individual collectors? Where can they store their NFTs and what is the best way to do so.

Software wallets

Software wallets are desktop and mobile software applications that store tokens like cryptocurrencies and NFTs. They’re also commonly called hot wallets because they connect to the internet and have private keys stored online.

Software wallets are definitely the most prevalent wallets storing NFTs due to their accessibility, especially for newer users. MetaMask, an Ethereum software wallet, is the most popular and is practically synonymous with software wallets. Of course, there are other Ethereum hot wallets like Trust Wallet and Coinbase Wallet, as well as non-Ethereum software wallets like Phantom and Sollet on Solana, and Temple and Kukai for Tezos.

The big issue with software wallets is that their online connectivity makes them much more vulnerable to malicious actors. While it may feel that a 12-24 word seed phrase makes these wallets pretty secure, that has turned out to be far from the case.

Countless MetaMask users have had their hot wallets compromised by online phishing scams, or by unknowingly downloading malware while browsing the internet or by clicking on malicious links. Unfortunately, it’s the thing that makes hot wallets convenient that exposes them to many different kinds of attacks.

Luckily there is an alternative that greatly reduces the risk of losing your NFTs to scams.

Hardware wallets

If this sounds like the opposite of a software wallet, that’s because it is. A hardware wallet is an actual physical device, often resembling a USB flash drive. Like software wallets, hardware wallets can allow users to store both cryptocurrencies and NFTs.

A popular misconception is that hardware wallets store tokens. In reality, a hardware wallet simply controls the private keys to a wallet, taking them completely offline. Hardware wallets carry multi-word seed phrases and tend to be password-protected on top of that.

Hardware wallets are a huge step up from software wallets because private keys on a hardware wallet never connect to the internet. In other words, they’re not susceptible to being stolen outright. The only way to hack a hardware wallet would be to attain the physical device, as well as the password/associated private keys. Not impossible, but far more difficult than hacking a software wallet.

As far as what hardware wallets people use, the most popular options come from industry leader, Ledger. In particular, its Ledger Nano X and Nano S may well be the two most used hardware wallet options for NFT owners.

In truth, all NFT owners trading anything of any value should really be using a hardware wallet. Or at the very least to store their higher value NFTs. After all, you can pick up a good hardware wallet for under $100 – a small price to pay to protect hundreds or thousands of dollars worth of assets.

Ledger, the most popular hardware wallet

Ledger’s security comes from the fact that it stores your key in a certified secure chip, which only you can access. This security certification, in itself, comes from the French cyber security agency, ANSSI. Reportedly, Ledger is the only hardware wallet certified for security.

The Ledger wallets come in the size of a USB drive and have stainless steel coverage, making them easy to carry as well as resistant to mechanical shocks. Their display screen, which cannot be tampered with or hacked, allows you to always ascertain that you are signing a genuine transaction. These wallets are also available in a range of colours, including even a “see-through”, transparent option.

Additionally, Ledger’s hardware wallets are accompanied by an app called the Ledger Live app. This combination of hardware and software enables you to safely, and securely manage your assets. In other words, the app makes it convenient and easy to manage thousands of coins and tokens from your devices, while enjoying the security of a hardware wallet.

“We recently integrated NFT management within Ledger Live, to allow you to secure, visualize, and use your NFTs from within the Ledger Ecosystem,” the Ledger team notes. Moreover, the app enables you to send and receive tokens, review your portfolio, and exchange tokens, to name a few functions.

As mentioned previously, Ledger Nano X and Nano S are the most popular products from the company. The former is well-suited for crypto enthusiasts who have a lot to store. It supports over 100 apps and costs $119. Nano S, on the other hand, is the least costly product from Ledger. But, it only supports installing up to three applications, because of which it’s preferred by those who trade in few tokens and assets.

Meet the new Ledger Nano S Plus

That’s not all. After much anticipation, Ledger recently launched the new Ledger Nano S Plus, an upgraded version of Nano S. The highlight of Ledger Nano S Plus is NFT integration. With NFT integration, you can always see the full details of your NFT transactions, including the collection and what you’re sending, whenever you transact through Ledger Live.

Apart from this, it has a larger screen, more memory, and supports more assets. All in all, the device can manage around 5,500 digital assets and over 100 apps. This device will cost you $79.

How to keep stored NFTs safe

In summary, it’s each collector’s responsibility to care for their NFTs. For now, the safest personal storage options are hardware wallets, which are a necessity if you’re serious about investing in NFTs.

However, experts do agree that we need to address this issue as soon as possible:

“This is definitely a long-term issue that the ecosystem will have to figure out,” says Foundation platform developer Elpizo Choi.

If you don’t want to (or can’t) get a hardware wallet, make sure to set elaborate passwords, and stay away from shady websites or NFT projects. All in all, there are many things to keep in mind to keep your digital assets safe amid the current NFT craze.

All investment/financial opinions expressed by NFTevening.com are not recommendations.

This article is educational material.

As always, make your own research prior to making any kind of investment.